Trends in Dentistry

Exploring the developments impacting the clinical side of the profession

Jason Mazda

Maintaining an awareness of trends among your clientele is important in any profession. In dentistry, how many general practitioners are placing implants? How many still work with amalgam? How many have adopted digital impression scanning? How many utilize websites, social media, online reviews, and more? Using readership surveys from Inside Dentistry and interviews with key opinion leaders across various disciplines, IDT answers those questions and many more, identifying 2020's Trends in Dentistry.

COVID-19, undoubtedly, was the predominant trend of 2020. Just a few weeks after thousands in the industry gathered in Chicago, Illinois, for the annual Midwinter Meeting and surrounding events, dentistry ground to a halt as the ADA advised practices to limit their work to only emergency cases during the early height of the pandemic. Unsurprisingly, the impact of COVID-19 is ubiquitous, from the projected proliferation of private insurance to an increased demand for cosmetic services that at least one leading dentist attributes to the frequency of videoconferencing this year.

"COVID-19 advanced the dental industry 5 years in 5 months," says Roger P. Levin, DDS, CEO of the Levin Group.

Many trends, however, can be attributed primarily to developments in technology, materials science, changing attitudes and philosophies within the profession, and other factors. For example, COVID-19 does not seem to have slowed the adoption rates of digital intraoral impression scanning, cone-beam computed tomography (CBCT) imaging, chairside milling, and in-office 3D printing.

"We are not far from a time when anything besides digital technology is unimaginable," says M. Reed Cone, DMD, MS, CDT, FACP, a prosthodontist in Portland, Maine.

Business of Dentistry

The most powerful economic driver in dentistry is probably private insurance, which 86% of the dentists surveyed say they accept. Membership plans have emerged as challengers in recent years, and 48% of dentists surveyed now offer them, but Levin says these options will merely supplement private insurance, not replace it. The Levin Group Data Center projects the number of dentists accepting private insurance to reach 94% to 95% by the third quarter of 2021.

"Insurance companies are big, well-capitalized, and powerful; they are not going anywhere," Levin says. "This was a trend we anticipated, but it is accelerating as we hit a rougher economy in the COVID-19 era."

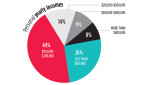

Despite the pandemic's economic implications, 86% of dentists surveyed say the yearly net income of their practice is more than $100,000. Among individuals, the safest bet seems to be working for DSOs, while independent practice presents higher risk but higher rewards. Only 8% of DSO dentists surveyed say they make less than $100,000 in personal income, while 67% make $100,000 to $200,000; among independent practitioners, 27% make less than $100,000 but 31% make more than $200,000.

Levin anticipates that DSOs will become a viable long-term career path for more dentists in the future, but also that they will continue to serve as a stepping stone for some.

"More dentists will find the financial stability of working for a DSO appealing at a young age as they pay off student loan debts; as they get their lives going, they might not want to take the risk of opening their own practice," Levin says. "However, I do still talk to many young DSO dentists who see it as an opportunity to gain experience while paying off debt, and intend to start or join a private practice in 3 to 5 years."

Business models for practices vary. For example, 13% of dentists surveyed work with a practice management consultant, and 29% say they spend more than 2 hours per month on staff training.

"For every dollar businesses spend on training, they recoup $3 to $5," Levin says. "Dental practices are highly focused on production, which I endorse, but if you do not spend time on training, then you are dependent on the economics. In a good era such as 2019, you can do fine. Post-COVID, you need to access the full potential of the practice."

Another way to access that potential is through marketing. One-quarter of dentists surveyed say they use outside professionals to create their marketing materials, 64% use social media for marketing, and 74% use a practice website. Social media is a more popular strategy among dentists in practice for 5 years or fewer (76%) than those in practice for more than 10 years (58%).

"Social media can depend on the platform, so understanding the different platforms is important," says Adamo Notarantonio, DDS, FICOI, AAACD, a private practitioner in Huntington, New York, who has nearly 15,000 Instagram followers. "I get some patient referrals from Instagram, but Facebook accounts for more because the demographic is different; it is a bit more family-oriented."

Levin says 65% of patients visit a practice website prior to or after making an appointment, and that 50% of patients who say they found a practice online actually did not.

Online reviews can make a tangible impact on a practice as well—even if 73% of dentists say referral by established patients is a more significant source of new patient appointments. Levin worked with one practice that had only 10 reviews, and simply by learning how to ask patients for reviews, they got more than 200 and their new patient numbers increased by 20%.

Brooke Blicher, DMD, an endodontist in White River Junction, Vermont, says her own research shows that patients use online reviews to supplement personal recommendations.

"People take the word of someone they know, but then they often look up reviews to make sure nothing negative is out there that their acquaintance just did not know," Blicher says. "As a specialist, I even hear from patients that they look up our reviews after being referred by another professional."

Cone says most, if not all, of his practice's new patients say they looked online and saw positive reviews.

"Dentists underestimate how savvy their patients are," Cone says.

In the Chair

As important as marketing is, patient demand is another critical part of the equation—especially for cosmetic dentistry. Anecdotally, Notarantonio says demand seems to be increasing due to the proliferation of videoconferencing during the pandemic.

"We have had patients say, ‘I see myself on a screen more than ever, and it bothers me,'" Notarantonio says. "I was a bit shocked by that, but my associate has heard it also. When you look at something over and over that you never looked at previously, you can become more self-conscious."

An increased demand for cosmetic dentistry would at least partially explain why the percentages of dentists offering various bleaching services increased from last year's survey, with custom trays going from 61% to 76%, chairside whitening 20% to 47%, go trays 5% to 21%, stock whitening trays 3% to 8%, and strips 2% to 9%.

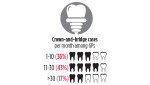

General practitioners are widely performing specialty services as well, with 69% of those surveyed saying they place implants and 76% saying they perform endodontic procedures. Opinions vary on the subject of implant placement.

"Most of the implant work that I do as a specialist is fixing other dentists' work," Cone says. "Implants can be very challenging even for specialists. There are real people attached to the end of these titanium screws, so decisions should not be made for primarily financial reasons."

Timothy F. Kosinski, DDS, MAGD, who has been placing implants since 1984, says the keys are proper training and knowing your limits.

"Anybody can put a screw in a jawbone, but few can place it in the perfect position," Kosinski says. "It requires more than just a weekend course. You need to understand what you are doing—and what you cannot do. I place 1,200 implants per year, but I still refer a lot to my oral surgeon and periodontist. Particularly in the anterior, you cannot make little mistakes without potentially ruining somebody life."

Maria L. Geisinger, DDS, a Professor in the Department of Periodontology at the University of Alabama at Birmingham, says anyone placing implants must be aware of the various considerations involved.

"There is a strong economic driver to place implants," Geisinger says, "but the caveat is that we need to set ourselves up for success as a profession and thinking about what we can do for the betterment of the patient, reducing the risk of implant complications—in particular, peri-implant diseases, which have been reported in as many as 47% of all dental implants that are placed—really requires a comprehensive view of the patient. My colleague at UAB, Nicolaas Geurs, DDS, MS, likes to say dental implants should be restoratively driven and biologically executed. If we understand both the restorative components and the underlying biology, that really informs the types of treatment we should be providing. Thus, implants should not necessarily be the purview of any one specialty, but there should be required learnings and trainings necessary to perform implants; in many cases, implant site preparation procedures, including both soft-tissue grafting and restorative components, are critical to ensure the long-term success of implants."

One of the first decisions to be made when planning implant treatment is to utilize screw or cement retention. In last year's survey, 66% of dentists said they place cement-retained implants and 61% said they place screw-retained implants. This year, 64% say they use screws and only 53% say they use cement. Kosinski says the push toward screws has been driven primarily by a desire to avoid periodontal problems cause by cement in the sulcus, but that screw-retained implant crowns also are significantly less expensive.

"However, you can only utilize screws when the angulation is proper," Kosinski says. "The other disadvantage is needing to cover the access hole with composite, which does not look quite as good."

Screw retention, of course, offers benefits besides affordability and avoiding peri-implant complications.

"I really like the retrievability of screw-retained implants," Cone says. "If the occlusion is managed properly—and this is where working with a good laboratory technician is important—that is a much better option."

Tools of the Trade

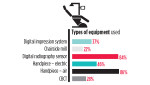

No discussion of dentists' capabilities for certain procedures would be complete without addressing the products at their disposal. For example, CBCT has dramatically increased diagnostic and planning abilities for implants, endodontics, and more. Among dentists surveyed, 28% overall say they have CBCT in their practice, up from 22% last year; 60% of those working for DSOs have it.

Digital impression systems are used by 37% of dentists surveyed, including 52% of those in practice 5 years or less and 43% among DSOs and small group practices. The overall number was 36% last year.

"Especially with COVID-19, companies are marketing digital impressions as a safer, more sterile method," Cone says. "It is important to remember, however, that this should not be a shortcut or a proxy for good preparations."

Dennis Urban, CDT, Vice President of Education and Training at Dental Services Group (DSG), says he observed "a dramatic increase" since the second quarter of 2020 over the previous year.

"I expect the trend to accelerate," Urban says, "not just with digital-savvy dentists but also with more experienced dentists who are getting more comfortable with digital technology."

The cost of entry still can be prohibitive for dentists of any experience level, however, as noted by Lee Culp, CDT, CEO of Sculpture Studios in Cary, North Carolina.

"Some leading scanners have all-in prices approaching $65,000," Culp says. "The prediction is always that next year will be when scanning adoption takes off, but we have yet to see that happen, and I anticipate the growth to continue very slowly."

Similarly, chairside milling is up from 15% last year to 22% in this year's survey, including 27% among both DSOs and dentists in practice for 5 years or fewer.

"For DSOs and dentists who want to mill, it makes sense," Culp says. "For the average dentist, a 1-hour crown might seem attractive, but they quickly learn that everything needs to be executed perfectly in order for that to be the reality. As a result, we still see a lot of mills being purchased and then not used on a regular basis."

Urban, who is the 2020/21 NBC Chair, says many dentists he speaks to simply prefer to leave laboratory work to laboratories.

"Even on single-unit cases, dentists like working with laboratories," Urban says. "There is more communication than ever, and we offer technical and material support as well."

Urban adds that an increase in in-house laboratory technicians at dental practices could contribute to a rise in the popularity of in-office milling. That would address some of the financial challenges involved with milling, which Notarantonio says are a result of insurance reimbursements typically being higher for chair time than for laboratory work.

"My office is 100% fee-for-service, so I can charge whatever I want; taking the time to mill a restoration and put it in the oven does not impact my overall production," Notarantonio says. "In offices that need high patient turnover rates, it might not work."

When purchasing new products, KOL recommendations are the most popular sources for research and evaluation, according to the survey. Clinical research was listed as being paramount or very important by 78% of dentists in practice for more than 10 years vs 59% of those in practice for 5 years or fewer.

"Many experienced dentists have been burnt with early adoption of products or techniques that ended up being less than ideal," Geisinger says. "Individuals now can obtain information from a wider variety of sources, such as YouTube and Instagram, but ideally, peer-reviewed clinical research that demonstrates clear benefit is preferable. Still, it takes time to achieve that level of evidence, and we often need to make decisions based on the best evidence available."

Collaboration

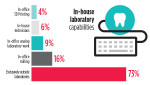

Of course, dental laboratories often serve as valuable resources themselves for dentists. Among dentists surveyed who do indirect restorative work, 73% say they exclusively use outside laboratories, 6% employ a dental technician, and 29% say they do at least some of their own laboratory work. Only 12% say they send any of their work overseas—knowingly, at least.

"New tariffs on China and the COVID-19 situation could explain 88% of dentists trying to keep their laboratory work in the US," says Renata Budny, MBA, CDT, MDT, an Associate Professor at New York City College of Technology. "Many dentists did not know their cases were being sent to China, and it was a crude awakening. We will see many changes and a large amount of work being retained in the US for that reason, as dentists hopefully appreciate the work of technicians in the US."

Still, most states do not require laboratories to disclose whether work is being done overseas. In that regard, dentists' expectations for outside laboratory work might be at odds with reality. Despite the efforts of the National Association of Dental Laboratories (NADL), only eight states require dental laboratories to register with the government, and 11 require point-of-origin disclosures. However, 87% of dentists surveyed say they believe laboratories should be required to register and/or disclose point of origin. Additionally, 76% say it is either paramount or very important to use a laboratory whose technicians are CDTs, and 73% say it is paramount or very important to use a laboratory whose technicians graduated from an accredited dental technology program.

"In reality, very few dentists ask about CDT certification, formal education, regulation, or disclosure," Culp says. "Formal education is voluntary. The US dental laboratory market is cowboy land because, in most states, anybody and their brother or sister can open a laboratory tomorrow with no regulation, certification, or licensure. The best chance of the profession being elevated by regulation is likely the FDA's increased attention on CAD/CAM production of laboratory products."

Urban says CDTs and graduates of accredited programs could market themselves more.

"I have heard from dentists all over the country that they feel more comfortable working with CDTs because of their knowledge and the continuing education required to maintain their certification," Urban says. "With the COVID environment, a CDT designation is even more valuable, because CDTs need at least 1 hour of regulatory standards CE per year."

Still, Budny says many laboratories and dentists do recruit talent from the NYCCT program and others like it.

"The value of a technician who has gained knowledge and experience from an accredited program and knows the fundamentals is increasing with new regulations," Budny says.

Dentists themselves hold the key to establishing more state regulations. The support of state dental boards and associations is usually required in order to pass legislation to regulate laboratories.

"Dentists can help this objective be achieved by reaching out to their state dental society leaders and government affairs staff, and encouraging them to make dental laboratory registration and disclosure part of their agenda," Urban says. "Historical data show that the notion of dentists' laboratory costs increasing in regulated states has been a misconception. We are headed toward more regulation in various states, and I anticipate a positive increase in years to come."

Another objective among leaders in the dental laboratory profession has been to elevate the federal classification of the profession from O*NET Job Zone 2 to Zone 3. When presented with the comparable jobs in those respective zones, 90% of dentists say the skill level required for a dental technician should be compared with O*NET Job Zone 3.

"I could not be happier to see that," Budny says. "If we could get dentists' support throughout the process of trying to make that change, it would be extremely helpful."

Dentist-laboratory collaboration seems to be on the rise; 26% of dentists say they communicate face-to-face or by phone with the laboratory prior to delivery of restorations for most of their cases, and that number rises to 60% among dentists in practice for 5 years or fewer. Similarly, 13% say they send full-face photography on most cases, and that number jumps to 40% among those in practice 5 years or fewer.

"As digital technologies become more widely utilized, especially in schools, dentists and technicians are increasingly aware of the value of digital collaboration and cooperation in general," Budny says. "Even using platforms such as FaceTime, Zoom or others can lead to better outcomes on complex cases."

Conclusion

As dentistry progresses into 2021, IDT and Inside Dentistry will continue to monitor trends in the profession for next year's installment of Trends in Dentistry. Undoubtedly, COVID-19 will continue to make its impact felt.

Levin believes one of the most significant developments in the next 3 to 5 years will be a staffing shortage, followed by a phase of bringing a large volume of new people into the profession.

Throughout these and other changes in an ever-evolving profession, running an efficient business with clinical philosophies, products, and partners that best fit each respective practice will be critical to future success.